The Fed Prisoner's Dilemma: Sell Now Or Keep Dancing?

Disclosure: The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Summary

- The Fed is likely to announce the end of QE3 in October, only 100 days away.

- Following the end of QE1 and QE2 we saw large corrections in the market.

- It appears that big money investors are already rotating into more defensive areas, preparing for more difficult times ahead.

[Joe Kernen: You have been on Squawk Box and said as long as -- you sound like Chuck Prince. You're still dancing now basically. Until they raise rates you're going to dance, right?

Stan Druckenmiller: First of all, I'm not like Chuck Prince because I can get out. I am still dancing, but Chuck Prince and the Fed, if they're wrong, cannot get out. I can get out in a week.] - CNBC, July 17, 2014

Some of you may be familiar with game theory and the famous example of the Prisoner's Dilemma. In the game, two members of a criminal gang are arrested, imprisoned, and isolated. They have two options: 1) cooperate with one another (stay silent), or 2) betray one another (testify that the other committed the crime). The various payoffs for each decision can be seen below.

(click to enlarge)

The dilemma is as follows. From a purely self-interest perspective, it is in each prisoner's best interest to defect as they have the opportunity to go free with the other party serving 3 years if other party stays silent. However, as both prisoners are likely to pursue this self-interested option, they are collectively worse off, with each prisoner receiving 2 years in jail. Had they cooperated and remained silent, they would have each served only 1 year in jail, the best possible combined outcome.

The Fed Prisoner's Dilemma

Many market participants today are faced with a similar dilemma, and they have become prisoners, in recent months, to Federal Reserve policy. After five and a half years of 0% interest rates and three rounds of QE, returns on virtually all asset classes have been pulled forward. This is precisely what the Fed intended to happen as Ben Bernanke made clear in his famous "wealth effect" Op-ed in 2010.It is debatable whether there has indeed been a "virtuous circle" as Bernanke suggested, where higher stock prices were supposed to "spur spending" and "lead to higher incomes and profits."

What is not debatable is that bond yields are at/near all-time lows while stock prices are near valuation highs. This suggests that forward returns from here are likely to be significantly below average. As such, market participants are becoming increasingly reliant on the Federal Reserve to maintain the status quo, and to not pullback from unprecedented measures even five years into a recovery. For if asset prices are elevated in large part because interest rates are artificially low, it stands to reason that if interest rates are no longer held down asset prices will have to fall.

The dilemma today is as follows. We know that the end of QE3 is fast approaching in October, as the Fed indicated in its most recent minutes. We also know that following the end of QE1 in 2010 and QE2 in 2011 we saw correction of 17% and 21% respectively in the S&P 500 (NYSEARCA:SPY).

(click to enlarge)

It is impossible to quantify how much of a premium the market is trading at with the psychological support of QE underneath it, but let's assume based on the action in 2010 and 2011 that it is at least 15% higher than it would otherwise be.

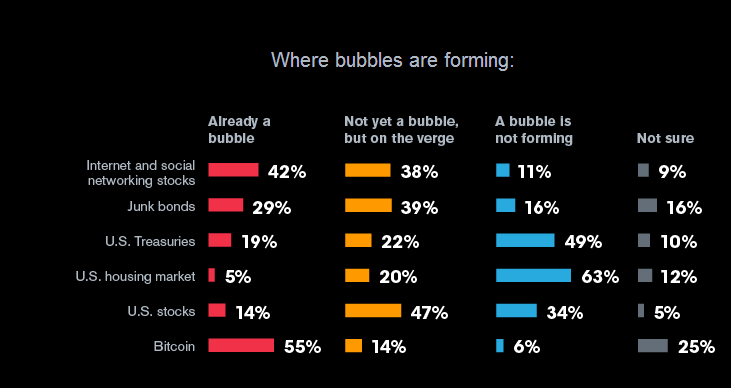

Now, we know that institutional investors are not oblivious to this and we also know that they understand that valuations are getting stretched at current levels. In a recent poll of investors, Bloomberg found that 47% of those surveyed believed the equity market was close to "unsustainable levels" while 14% already saw a "bubble." In the high yield bond market, it the results were even more alarming, with 70% of those surveyed saying the rally in junk-rated bonds was "in a bubble or close to one."

(click to enlarge)

Source: Bloomberg Poll

Two Hedge Fund Managers Walk into a Bar

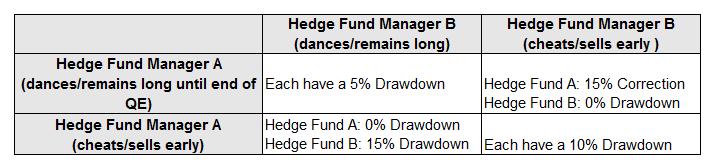

Say we have two hedge fund managers and they are the only active market participants: Hedge Fund Manager A, let's call him Davy Tepper, and Hedge Fund Manager B, let's call him Billy Ackman.Davy and Billy are both heavily long equities and well versed in QE and what happened in 2010 and 2011. While they are both still very bullish on equities, they do not like drawdowns and neither do their investors. They are aware of each other's existence but are isolated in the sense that they don't speak to one another before they make a trade.

What are their options here with the equity markets at all-time highs and the end of QE fast approaching? They can 1) remain heavily long (dance until the music stops) and wait until the end of QE to sell, or 2) cheat and sell early while the music is still playing.

A theoretical payoff diagram is below. If Davy and Billy cooperate and stay long, they can have a nice, orderly sell-off at the end of QE with a 5% drawdown. However, Davy doesn't like 5% drawdowns and neither does Billy. They both would prefer a 0% drawdown and have the other fund suffer a 15% drawdown. They would look like heroes in that scenario. By acting in their own self-interest and selling early, though, they will end up suffering more than had they cooperated, each incurring a 10% drawdown.

(click to enlarge)

Now I realize that this is a wild hypothetical and many ridiculous assumptions are involved, but let's think this through for a second.

If one wanted to cheat and sell early what would be the main risk? A market that continued to move higher whereby one would miss out on gains, of course. As we all know, the cardinal sin in hedge fund investing is missing out on upside, even it's in the very short term. If everyone is down and you're down too, that's fine; but if you're flat when everyone else is up that's a one-way ticket back to the sell-side.

How to Keep Dancing Without Going to Cash

Is there a way that one can sell early without suffering the consequences if the market continues to rally for some time? Sure, by subtly adjusting one's beta, or reducing one's risk. And if I wanted to reduce risk without other funds knowing about it, I would do three things:1) Move out of more illiquid/higher beta small and micro caps and more liquid/lower beta large caps,

2) Move out of more cyclical sectors like Financials and Consumer Discretionary and into more defensive sectors such as Utilities, and

3) Move into one of the most defensive asset classes, long duration Treasuries.

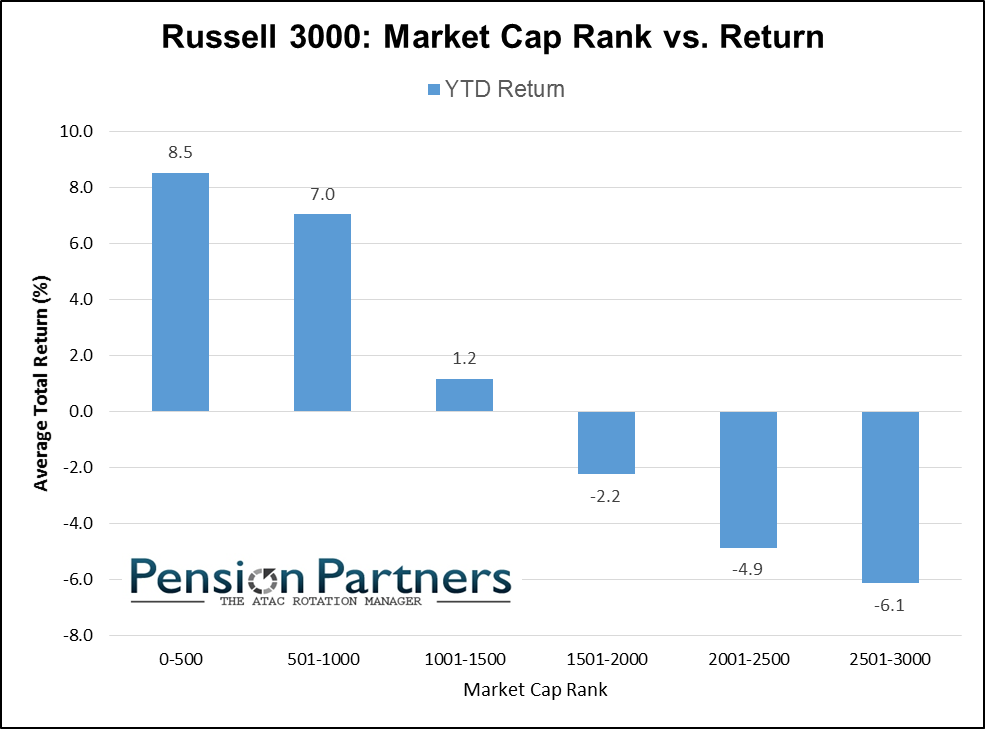

If we look at the markets in 2014 we can clearly see that many funds are likely already cheating in some form.

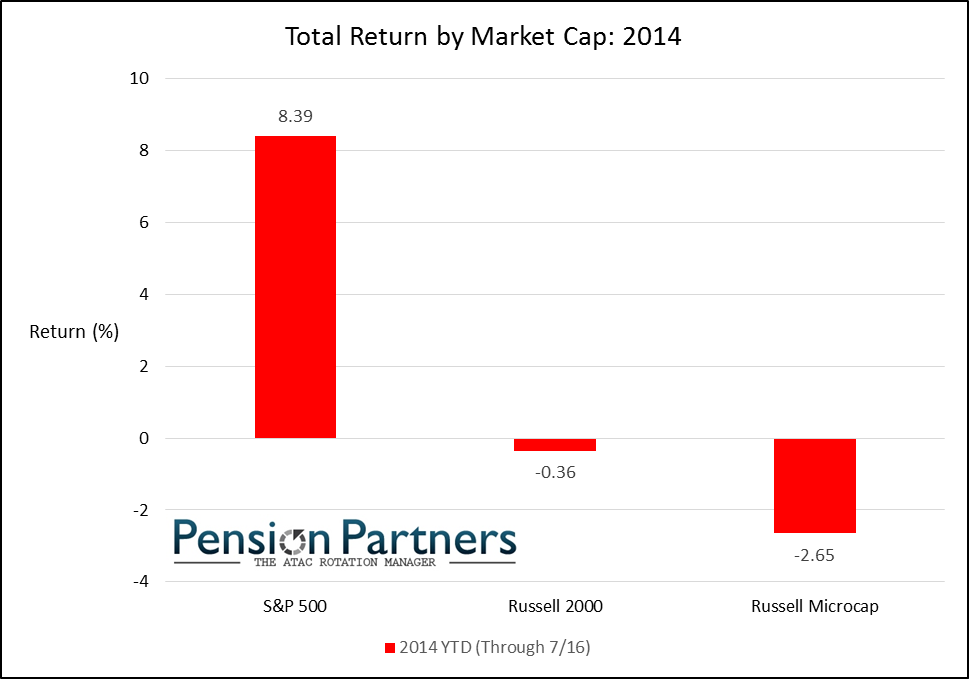

First, as I wrote about last week, there is a glaring divergence between large and small cap stocks, with the S&P 500 and Dow (NYSEARCA:DIA) still hitting new all-time highs while the Russell 2000 (NYSEARCA:IWM) and Russell Microcap (NYSEARCA:IWC) indices are down YTD.

(click to enlarge)

(click to enlarge)

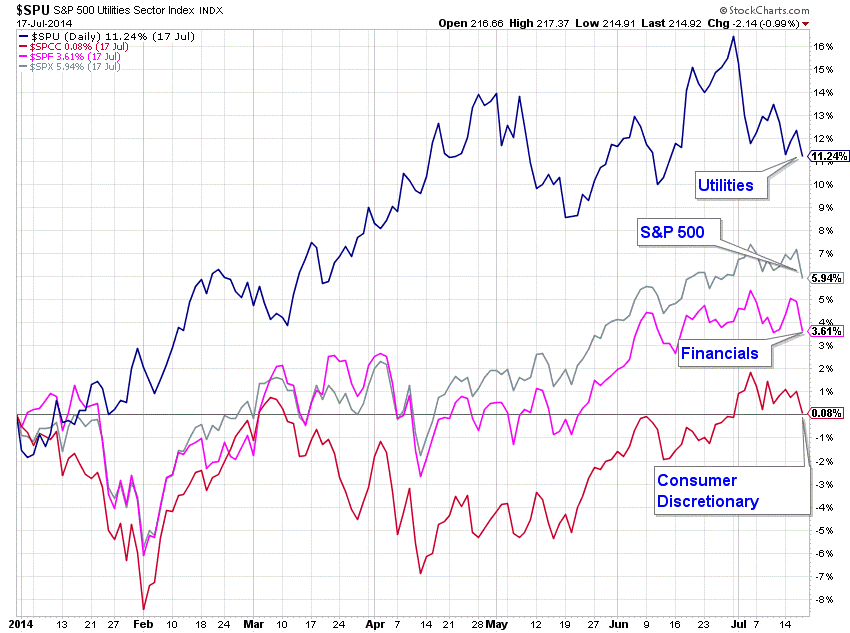

Second, we are seeing classic late cycle behavior within sectors, with the defensive Utilities (NYSEARCA:XLU) sector outperforming while the cyclical Financials (NYSEARCA:VFH) and Consumer Discretionary (NYSEARCA:VCR) sectors are underperforming. As I wrote about last week, this behavior bears an uncanny resemblance to July 2007.

(click to enlarge)

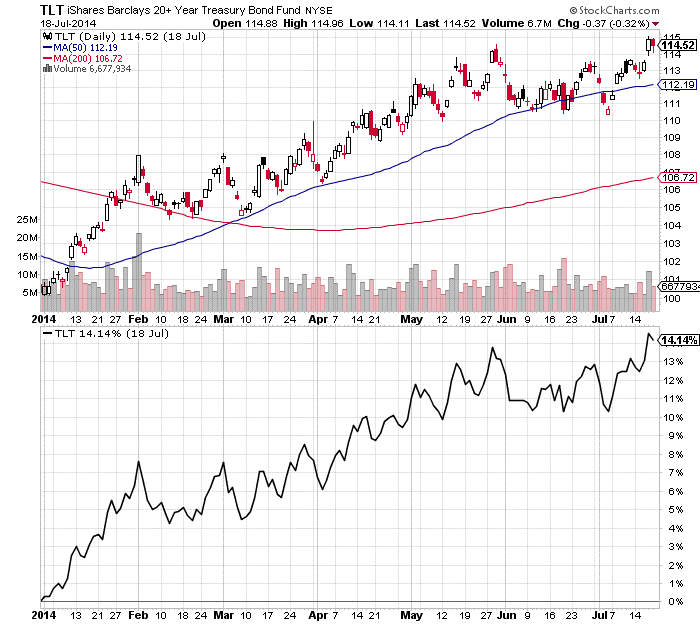

Lastly, we are seeing a persistent bid in one of the most defensive asset classes: long duration Treasuries (NYSEARCA:TLT).

(click to enlarge)

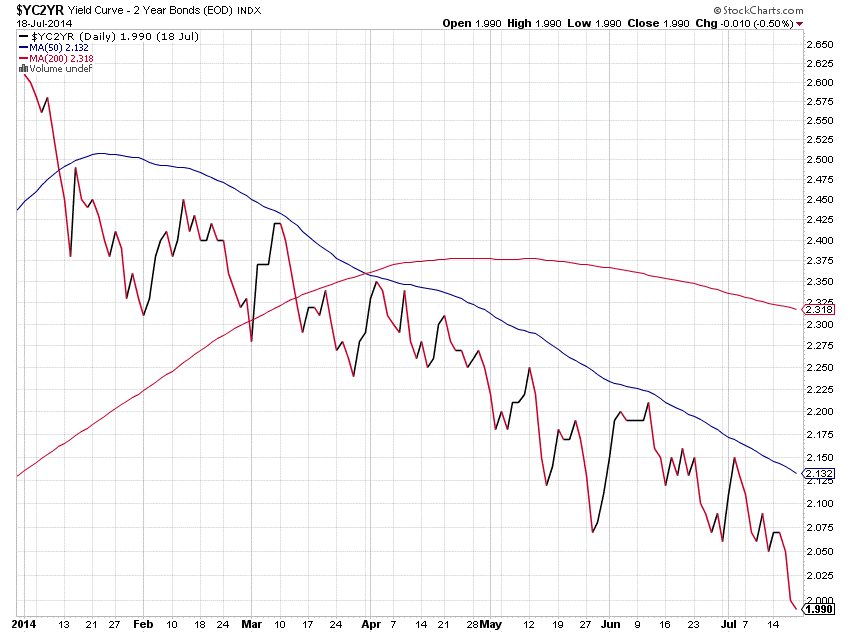

Not only are they outpacing US equities YTD, but the yield curve has been flattening the entire year, an additional signal of defensiveness within the Treasury market.

(click to enlarge)

One Foot out the Door

Whether you subscribe to my Fed game theory or not, it is important to recognize what the market is telling us. In no uncertain terms, the big money investors are already preparing for more difficult times ahead with "one foot out the door" rotations into lower beta areas of the market. They may not be going to cash as they still fear missing upside, but they are certainly not going to wait for the end of QE to reduce risk in their portfolios.Many investors will disregard this message that the market is sending, as they are probably thinking that they are like Druckenmiller and "can get out in a week." Perhaps, but if the events following 2000 and 2007 have taught us anything, investors are much more likely to overstay their welcome than to sell early. There is now only 100 days left until the Fed's October meeting where they are expected to announce the end of QE. What will you do?

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

No comments:

Post a Comment