We are in the climax of Greece’s debt crisis. It has been a

slow-burn crisis, a five-year-long string of high-drama confrontations

amid tedious talks. These next three weeks are crucial. The endgame is

July 20, when Greece must repay a bond to the European Central Bank. Barring a last-minute U-turn by

Greek Prime Minister Alexis Tsipras to accept the economic policies

that Greece’s creditors are demanding as the condition of further

bailout loans, here is how that endgame would look.

What happens today, June 30?

The bailout program officially expires and a payment of €1.55 billion ($1.73 billion) to the IMF falls due.

Does that matter?

Barring a magical rabbit springing from a hat, Greece will miss the IMF payment. The IMF will be mad,

but the missed payment has few practical consequences. The eurozone

bailout fund has the option of declaring Greece’s rescue loans in

default and demanding accelerated repayment, but that would be a nuclear

option it likely wouldn’t exercise—at least not right away. The bailout

fund is controlled by eurozone finance ministers.

Greek banks have relied for months on emergency lending from

the central bank. They have scant cash and few assets they can quickly

sell, so when a depositor asks for a withdrawal, they must borrow from

the central bank to be able to give the depositor cash.

Greeks have made €35 billion in withdrawals this year through May,

the most recent available data. Non-Greek banks have pulled nearly

another €30 billion of loans. The Greek banks have less than €2 billion

in cash.

On Sunday, the ECB froze the emergency lifeline at around €89

billion. Unable to get more cash to give to depositors, banks shut

Monday. To reopen the banks, that lifeline needs to be turned back on.

Will it?

It is difficult to imagine the ECB increasing the lifeline

without the Greek government and the European creditors agreeing to a

deal.

The ECB is right now taking a middle course. Since banks need more

money every day to cope with withdrawals, freezing the lifeline shuts

the banks but doesn’t kill them. The lifeline comes in the form of loans

to the banks that are regularly renewed; in effect, the ECB is saying

you can’t have any more loans but we’ll keep renewing the ones you have.

The tougher course would be to end the lifeline entirely and demand that the loans be repaid when they come due.

Why might the lifeline end?

The lifeline, called Emergency Liquidity Assistance, or ELA, is highly flexible. The rules

say that the banks receiving it must be “solvent,” but otherwise the

ECB has broad latitude. The ECB also doesn’t lend for free—it has

required the Greek banks to post assets as collateral to get ELA.

So two things could kill the lifeline: Insolvency of the banks, or a

determination that the collateral they are posting isn’t adequate. Let’s

take them one at a time.

By the books, the Greek banks are solvent. They have assets,

primarily in the form of loans, that exceed their liabilities, primarily

deposits and central-bank lending.

That, of course, could change—perhaps many of their loans need to be

written off or reduced in value. Perhaps the deferred tax assets

(basically, promises that they’ll get tax refunds or credits in the

future from the Greek government) they hold aren’t worth as much as they

imagined.

The banks don’t have heavy holdings of Greek government debt: €13.8

billion out of a total assets of nearly €400 billion—even if that debt

went to zero the banks would probably remain solvent.

Collateral is another matter. The ELA is secured by a hodgepodge of

collateral: some of the banks’ loans, some covered bonds, a little bit

of government debt. For the four big banks, though, a special kind of

government-guaranteed bond makes up a large chunk of the collateral.

That means to keep ELA going, the ECB must primarily assess whether

the government’s guarantee is solid enough to make the collateral

adequate. It’s a judgment call.

So would bailout expiry end the lifeline?

Probably not, especially when there is a referendum scheduled

in five days. The ECB is loath to be seen as interfering in politics.

The formal end of the bailout program doesn’t directly affect the banks’

solvency. Some on the ECB’s board might argue that it hurts the

government’s guarantee and thus the adequacy of the special bonds. But

the ECB could credibly keep the lifeline frozen at least through the

referendum.

How much longer?

July 20. That day, €3.5 billion in Greek-government bonds held by the central bank fall due.

If Greece doesn’t pay, the ECB would be hard-pressed to keep ELA alive.

An actual payment failure makes the judgment call about the

government’s guarantee much clearer.

What happens if ELA is ended outright?

The banks collapse as soon as the ELA loans come due. The banks

cannot repay them. So the collateral they posted would be seized. They

posted more than a euro in collateral for each euro in lending, and thus

they collapse.

When would the famous “Grexit” come?

Right around then. It could be as soon as July 21, if the loans

granted under ELA are overnight loans (the exact maturity isn’t known).

If the banks have collapsed and there is no central-bank support, the

government would have to create a new currency to restart the financial system and make payments.

Can it be avoided?

Yes, but time is excruciatingly short. The referendum is July

5. If there is a “Yes” vote, Mr. Tsipras has hinted he would resign. A

new government would need to be formed, a deal signed, legislation

passed and money disbursed from the creditors in time to make the July

20 payment.

If there is a “No” vote, Mr. Tsipras would presumably try to

negotiate a better deal on the back of the popular support. And again, a

deal would have to be reached, legislation passed and money disbursed

by July 20.

Could the ECB forestall Grexit at the last minute?

If it wanted to be really, really, really nice it could come up

with a way to overlook a missed July 20 payment. Perhaps it could

invoke a grace period. And Standard & Poor’s, the rating firm, has

said a default on the ECB-held bonds would not be enough to place the

Greek government in default. (S&P says its ratings reflect a

borrower’s repayment of commercial creditors only.) Perhaps that’s

enough cover for the ECB to say the government’s guarantee is still

good.

But these are Hail Mary passes highly likely to be swatted down by the ECB’s board.

As China enters a bear market, it's become the No. 1 question on everyone's mind: Is this just a dip, like when equities fell 17 percent in mid-2007 before skyrocketing to an all-time high, or the start of something a lot worse, like the selloff that would begin just three months later and wipe 72 percent off the value of the nation's stocks?

After rallying more than 150 percent in the year through June 12, it took just five trading days for the Shanghai Composite Index to enter a correction, and five more for the bear market to form. With the central bank cutting lending rates and lowering reserve ratios on Saturday in an effort to revive investor confidence, where do we go now? Here's what 11 of the top analysts and investors in the industry have to say:

Wilmington Trust:

``A shares will continue to fall, on the basis of sharply negative speculative sentiment, as well as on the Chinese Securities Regulatory Commission's actions to control margin lending,'' Clem Miller, an investment strategist at Wilmington Trust, which manages $20 billion, said by e-mail June 29. ``The Shanghai Composite reached its current heights over the last few months based on leveraged speculation involving many uninformed retail investors. I expect the composite to fall by about another 20 percent.''

Janney Capital Management:

``Chinese equities should do pretty well going forward,'' Mark Luschini, chief investment strategist in Philadelphia at Janney Capital Management, which oversees about $68 billion, said by phone June 29. ``I don’t know at what level this correction may ultimately stop, but I think with the underwriting of the Chinese economy by the People’s Bank of China, Chinese officials don’t want to see the market nose down. They’ll do what it takes to push the market higher, and undoubtedly Chinese equities, post the correction, will work their way higher again.''

Marketfield Asset Management:

Mainland A shares could fall as much as 18 percent before bottoming, Michael Shaoul, Marketfield's chief executive officer, said in a June 29 report.

``Regarding the equity market itself the speculative rush into stocks would appear to have run its course, leading to a messy unwind,'' Shaoul said. ``We continue to find the offshore H share market to be a much more reasonable way to play a recovery of the Chinese economy.''

China International Capital Corp.:

``We see limited room for further correction in the short term. The market worried about the position closing pressure of margin holdings and the negative impact on market sentiment, but the interest rate cut and targeted reserve requirement ratio cut in the weekend sent out a signal of continuous loosening and removed the worries on possible marginal changes in policies, which could stabilize the market,'' CICC analysts led by Hanfeng Wang said in a June 29 report. ``Flexible money could start to position for a likely rebound.''

HSBC Holdings Plc:

``Policy support could prevent further sharp market falls; yet investors will likely sell into the rebound to lower leverage,'' Steven Sun, the head of Hong Kong and China equity research at HSBC, wrote in a June 28 note. ``We also think it would be premature to call an end to the policy-driven A-share rally, given the importance of the stock market in helping China’s state owned enterprises and key industries obtain much-needed financing, as well as the likelihood of more monetary easing.''

Bocom International Holdings Co.:

‘‘Large cap blue chips are still cheap, and their low valuation can be a good defense in the current market turmoil,'' Hao Hong, Bocom’s China equity strategist, wrote in a note on June 29. ``Our concerns are that the burst of the ChiNext bubble can create contagion onto other market segments, and the recovery of large cap blue chips will inevitably consume market liquidity bounded by a topping market cap/GDP ratio.''

Bank of America Corp.:

Rate cuts will ‘‘temporarily halt a possible crash in the market - had the government not acted, a stampede might soon develop as margin calls force leveraged positions to unwind,'' Bank of America Merrill Lynch strategists led by David Cui write in a June 28 note. ‘‘Short term bounce aside, we doubt that the latest cuts will trigger any sustained rally. There is still a small chance in our view that the bottom of the market may fall out in the coming weeks if enough investors conclude that the bull market is over - leverage is expensive so needs a consistently higher market to break even.’’

Central China Securities:

‘‘Panic selling will likely continue as margin investors are forced into liquidation and funds are forced into redemption after earlier heavy sell-offs,’’ Central China Securities strategist Zhang Gang said by phone June 29. ‘‘People are worried about further unwinding of margin positions.''

‘‘One single policy change isn’t going to reverse the market trend,’’ Zhang said. ‘‘And if the market continues with deeper falls, we will likely see more supportive policies’’

Invesco Ltd.:

‘‘It seems like policy makers are more worried about the stock market than about the real economy,’’ Paul Chan, chief investment officer for Asia ex-Japan at Invesco in Hong Kong, said June 29. ‘‘The economy is slowing down and they are so much behind the curve in terms of easing. But as the stock market corrected, they jumped in, putting in all the policies. It gives people a sense of panic.’’

Krane Fund Advisors:

``Ultimately if we could have a more pragmatic and incremental IPO schedule as well as the cutting back on the use of leverage, it is good for the stock market in the long run,'' Brendan Ahern, chief investment officer at Krane Fund Advisors, said by phone June 29. ``Why you want to invest in this market is the continued reforms of state-owned enterprises as well as that onshore equities will be included in the broader benchmark over time. The rationale for investment is still in place. We’re just working through some short-term issues.''

Marathon Asset Management:

‘‘There could be a substantial correction with China because it’s had a huge run-up,’’ Bruce Richards, co-founder of the hedge fund firm Marathon Asset Management said in an interview on the television program ‘‘Wall Street Week’’ that aired Sunday. ‘‘But in the long run, you have to figure out how you want to invest in China. There’s been lots of money to be made in U.S. equity markets over the last many decades -- the same exists in China.’’

--With assistance from Amanda Wang and Allen Wan in Shanghai and Kyoungwha Kim in Hong Kong.

China's stock markets tumbled on Friday to near bear territory further deepening the sell-off that started two weeks ago. The Shanghai Composite, down 7.4% on the day, has fallen 19% from its June 12 high wiping out $1.25 trillion in market cap. The smaller Shenzhen and ChiNet indices also have plunged 20% from their recent peak.

(click to enlarge)

Margin Lending Blessed by Beijing

Even with recent declines, the Shanghai Composite Index has surged nearly 30% year-to-date. Authorities have allowed local investors to borrow tons of money from brokers to speculate in the stock market (i.e., Margin Lending), while the central bank PBOC has cut interest rates three times since November. Beijing also introduced new easing measures in the past couple of days: a proposal to remove a cap on banks' loan-to-deposit ratio and injecting cash into the financial system.

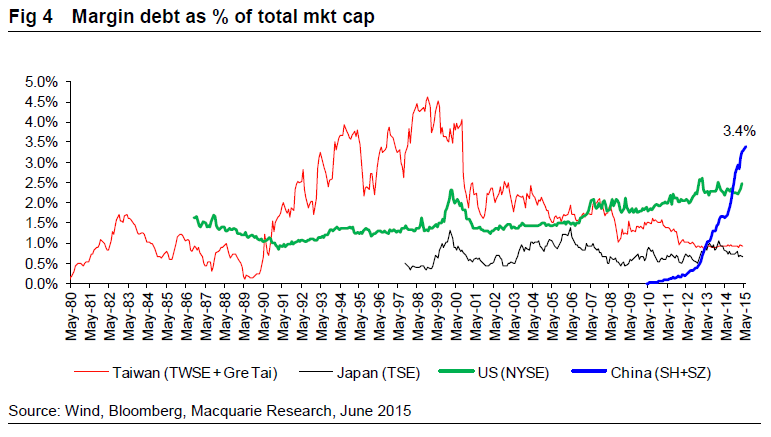

Margin Debt Soared to $370 Billion

Investors have poured into the market, opening 33 million new brokerage accounts between the start of January and the end of May. According to Macquarie Research, Chinese margin debt has risen 123% year-to-date, reaching a new record of 2.3 trillion yuan ($370 billion) on June 18.

Margin debt in China has reached 8.5% of the value of China's tradable shares (For comparison purpose, that ratio was only at 4.6% during the peak of the Taiwan Stock Market Bubble back in the late 80's).

(click to enlarge)

(click to enlarge)

Margin Debt Could Get Even Worse

It gets even better from there. Macquarie believed that the brokers should have enough capital available to push margin lending higher from here as reported by Bloomberg:

"We think that the peak should be somewhere around RMB 3 trillion and at the current run rate (i.e. +16% month-on-month) the market would reach that level around September."

Analysts Cutting Price Target

Investors have started to pull out of the market on concerns the government could be looking to rein in this debt-fueled rally. Meanwhile, more and more analysts are also sounding louder alarms about the over-heated China market. For example, citing concerns like valuations and high margin debt, Morgan Stanley just lowered its price target for the Shanghai benchmark in a report Thursday.

Plunge Leaves State Media Speechless

The usually quick-tongued state media like Xinhua are staying unusually quiet not giving out clues about the government's view on the current market sell-off.

Reuters quoted Zhang Xiaojun, a spokesman for the China Securities Regulatory Commission on Friday:

"It's a self-adjustment of the market after earlier excessive gains... Recently, there has been more volatility in the stock market. That requires all sides to treat it rationally."

Chinese authorities are already trying to discourage speculative bets on the highest-flying stocks. So these rare public comments from the Regulatory Commission seem to suggest authorities are 'comfortable' with the declines.

$370 Billion in Margin Trades

A stock market collapse would be devastating to China with slowing economy and during a difficult transition from a manufacturing-based economy to private-business-and-consumer-supported.

People are already freaking out that Greece is just days away from defaultingon a $1.72 billion loan payment. Just wait for the margin call on the $370 billion margin debt in China's stock markets should Beijing decide to take a page from Saudi Arabia's oil book.

With all the drama in the euro zone, there's been no shortage of Greece-related questions for Wall Street's luminaries.

Below

is a roundup of what big investors and banking luminaries have

been saying. The takeaway: Wall Street seems pretty sanguine when it

comes to Greece—perhaps surprisingly so.

Here's Warren Buffett, billionaire investor, speaking in March:

If

it turns out the Greeks leave, that may not be a bad thing for the

euro. ... If everybody learns that the rules mean something and if they

come to general agreement about fiscal policy among members, or

something of the sort—that they mean business—that could be a good

thing. —Interview with CNBC

Fink, CEO of BlackRock, speaks during the Credit Suisse Global Megatrends Conference 2015 in Singapore.

Sam Kang Li/Bloomberg

Larry Fink, chief executive of BlackRock, spoke with a Dutch newspaper last month and said:

A Greek departure from the euro is far less disastrous than making concessions that can also be claimed in other countries. —Interview with Het Financieele Dagblad

JPMorgan Chase CEO Dimon.

Tim Boyle/Bloomberg

Jamie Dimon, chief executive of JPMorgan Chase, wrote in his letter to shareholders in April that:

We

must be prepared for a potential exit. ... We continually stress test

our company for possible repercussions resulting from such an event. ...

After the initial turmoil, it is possible that a Greek exit would

prompt greater structural reform efforts by countries that remain. —Letter to shareholders

Weber, president of the Deutsche Bundesbank.

Hannelore Foerster/Bloomberg

Axel Weber, chairman of the Swiss bank UBS, said in April that:

I've

just come from a meeting of the International Monetary Fund. There, the

consensus is increasingly that a Greek default would be systemically

controllable. —Interview with Neue Zuercher Zeitung

Munger, vice chairman of Berkshire Hathaway.

Daniel Acker/Bloomberg

Charles Munger, vice chairman at Buffett’s Berkshire Hathaway, said in May that:

[The]

euro had a noble motivation and has done some good but has created

strains by connecting countries that shouldn't be. You shouldn't create a

partnership with your drunken, shiftless brother in law. —Berkshire Hathaway's annual shareholder meeting

Druckenmiller,

chairman and chief investment officer of Duquesne Family Office, speaks

during a television interview at the Robin Hood Investors Conference in

New York, on Nov. 22, 2013.

Peter Foley/Bloomberg

Billionaire investor Stanley Druckenmiller told Bloomberg TV in April that:

The

banks don't own Greek debt any more; Draghi has QE at his disposal. My

guess is there won't be contagion. But even if there is, he can contain

it—and as soon as market participants see that, you won't get contagion. —Bloomberg TV

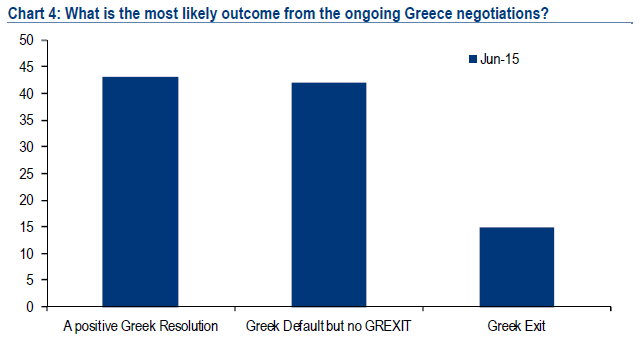

According

to a Bank of America Merrill Lynch survey released on Tuesday, many

investors are not anticipating a negative outcome in the euro zone.

Some

43 percent of respondents said they expect a "positive" resolution.

About 42 percent said Greece will default but is unlikely to exit the

monetary unit and only 15 percent said they expected a

so-called 'Grexit.'