In my last blog,

I wrote about my experience with building the SOFR curve. Now FINCAD F3

can handle any instrument market data for curve building. But at the

moment an important question is, “Which instruments are the right ones to use to build the SOFR curve?”

Right now, the market for SOFR-linked derivatives is just starting to

take shape, and market quotes are becoming available for CME SOFR

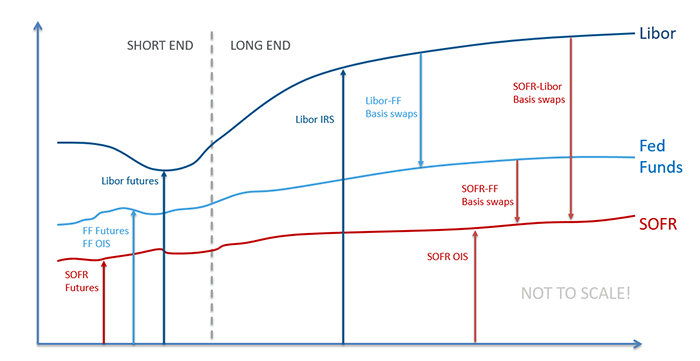

futures and SOFR swaps. There are three types of swaps that are being

traded: SOFR OIS, SOFR-FF basis swaps, and SOFR-Libor basis swaps. The

first one is an overnight indexed swap which pays SOFR versus fixed, and

the last two are basis swaps between SOFR and either the Fed Funds

effective rate (FF) or Libor.

The odd thing about introducing SOFR as an alternative benchmark

interest rate is that, for now, it makes the USD rate basis much more

complicated. This is because it adds two new basis spreads between

FF/SOFR and Libor/SOFR, in addition to the previous FF/Libor basis. So

now there are many possible ways to build the SOFR curve. These

include:

Single curve-building:

Use FF OIS to build the Fed Funds effective rate curve.

Use ED futures and Libor swaps to build the 3-month Libor curve.

Use SOFR futures and either SOFR OIS, FF/SOFR basis, or Libor/SOFR basis to build the SOFR curve.

Global curve-building:

Use ED futures, Libor swaps, FF OIS, FF/Libor basis swaps, SOFR

futures, and either SOFR OIS, FF/SOFR basis, or Libor/SOFR basis to

simultaneously build the 3-month Libor curve, Fed Funds effective rate

curve, and SOFR curve.

For many people, their instinct would be that building the

curves individually is the easiest. However, the dual dependence of the

FF OIS and FF/SOFR basis swaps on the OIS discount and SOFR curves

creates a curve construction problem, which necessitates a global

solver.

As mentioned in my previous post,

I chose to use the global method, because it is actually easier to just

let F3 automatically determine how to solve the curves from the

instruments selected. This approach also allows using the FF/Libor basis

for longer maturities, since often the Fed Funds OIS is not as liquid.

But there is still a big question here, “Which SOFR instruments should

we choose?”

Imagine swapping Fed Funds into Libor and then swapping Libor

exposure into SOFR. Now compare this with swapping Fed Funds into SOFR

directly. The question about the new SOFR basis is, “Does it roundtrip

so we get the same SOFR in both cases?” The answer right now is that

there is not enough trading on SOFR derivatives to closely round-trip

these two ways of swapping Fed Funds into SOFR. The symptom of SOFR

illiquidity is large bid-ask spreads in the market quotes for basis

swaps on SOFR, so that by using mid-quotes as market data, the SOFR

curve will look a little different in the two cases.

A recent summary of SOFR swap trading volumes

shows that there is a lot of uncertainty regarding where the volume

will show up in SOFR-linked derivatives. It is expected that they will

become traded more as time goes on, and competitive markets will result

in smaller bid-ask spreads. But we don’t know which swaps will be the

best to build the SOFR curve. Surely with Libor going away we shouldn’t

rely too much on Libor/SOFR basis swaps, but whether the future will

show volumes in the FF/SOFR basis or SOFR OIS is unknown. This is

another good reason to have a global curve-building solution which can

handle any and all instruments you throw at it. Such an approach will

help you react quickly to changes in trading volume in SOFR derivatives

to continue building the most accurate SOFR curve possible.

In case you missed it, you can check out my previous SOFR blog post here, “Building a SOFR Curve was Easy.” Also, be on the lookout for my next post, “Eliminating the SOFR Basis: What Do We Lose?”

About the author

Bin Hou

Senior Financial Engineer, FINCAD

Bin

is a member of the Financial Engineering Hub in Vancouver. Since he

joined FINCAD in 2013, Bin has made contributions to FINCAD products

through conducting model validations and encoding the best market

practice in examples and documents.

Bin holds a Master of Science in Finance degree from Simon Fraser University. He is also a CFA® and FRM® charterholder.

For which class of instruments the SABR/LIBOR Market Model does perform better than the classical LIBOR Market Model?

The LIBOR Market Model

The LIBOR Market Model — also known as Brace, Gatarek, Musiela model —

is an interest rate model capable of reproducing the correlation

structure of forward rates. One-factor models are unable to reproduce

this structure and therefore cannot price accurately derivatives whose

prices reflect these correlations. A typical example of such

derivatives are swaps paying a non-linear function of the difference two

swap rates for two different maturities.

The model is constructed by using a family of LIBOR rates: L0(t),…,Ln(t)

, where Li(t) is LIBOR forward rate starting at ti and ending at ti+1, following

dLi(t)=σi(t)Li(t)dWi+1(t).

The SABR LIBOR-Market Model

An important flaw of the LMM is known as sticky volatilities: if the model is calibrated in a highly volatile market it assumes that

this high volatility lasts forever, which leads to inaccurate results.

The SABR LMM attempts to address this issue. In this model, each LIBOR rate is assumed to follow a log-normal dynamic having stochastic volatility:

Tokenized Real Estate Lacks Features for Success.

Product-Market Fit Remains Deficient.

These Offerings Are Instructive in Seeking Better Offerings.

Tokenized real estate has long been discussed as a leading

use for digital securities. Yet, really no successful sales have taken

place. Some of the most notable and widely marketed projects were

pre-arranged to signal successful optics and had side deals to

incentivize investment. Though tokenized real estate will eventually

emerge, the benefits over existing financial offerings do not yet offer

the level of value needed to overcome market inertia and successfully

scale.

It’s no surprise that many real estate owners have an interest in

selling their property via a digital security fundraise. By

“fractionalizing,” breaking down investments into smaller pieces, real

estate sellers can ask for higher prices than they would selling

wholesale. Or alternatively, those that can not find buyers in

traditional markets turn to digital securities as a last resort à la

adverse selection.

Though this looks attractive to sellers, who would buy these

offerings? Consider the typical profile of a real estate investor -

conservative, interested in wealth preservation, sensitive to margin

costs. Generally, they do not want what most perceive to be experimental

investment technology. Furthermore, with the extant availability of

public REITs, fund managers, real estate crowdfunding,

and direct investments, the benefits of liquidity and access to foreign

inventory espoused by many security token evangelists are already

available. The short-term benefit to the investor is marginal at best

and comes with a high degree of perceived technology risk.

Ultimately, the real estate asset class suffers from the lack of high

upside to achieve product-market fit. A great real estate investment

for a passive investor might yield 20% a year. Why take all of this

perceived risk and adopt a new behavior when available investments can

offer similar returns without the unknowns? Due to adverse selection,

existing public and private market dynamics, and investor

characteristics, it’s hard to find a scenario by which both sides of the

transaction could find value meaningful enough to exceed the threshold

for adopting a new behavior.

The pool of digital security investors today is small and comprised

of, predominantly, blockchain/ICO-savvy investors. These people, still

nostalgic for their +1000% 2017 returns, have a high-risk tolerance,

want high-returns, and understand technology. They don’t want an 8%

fixed-income real estate debt product.

The primary exception to this may be those in countries with tight

capital controls (aka China), that want to expatriate their wealth into

stable, foreign assets. In this case, the primary benefit of security

token real estate, in short, is the ability to hide the movement of

capital from their government. I don’t know about you, but hiding cash

for the wealthy and circumventing national governments is not why I got

involved with blockchain.

Though real estate digital securities remain weak, their use-case

provides a helpful tool in exploring what a good investment would look

like. A “good” deal must benefit both parties in a transaction. The

product-market unfit of Real Estate and Security Tokens raises the

question of what, currently, a good deal would look like? What is the

ideal security token?

Ideally, digital security or not, the best investment has no risk and

infinite upside. Though such a perfect investment is unattainable,

features like downside risk protection (which can take many forms), a

known industry, and available liquidity can help to move an offering in

the right direction. At the same time, blockchain-based ownership needs

to offer some unique capability that necessitates a digital security

approach. This could take the form of high-complexity financial

structures, streamlined asset diligence, or blended “utility token”

benefits offering added value. This isn’t real estate.

Revenue streams backed by equity or a bond or other conversion

options may offer one strong example. In this case, a company may offer

investment into a new product-line or intellectual property asset and,

if the upside doesn’t manifest (as measured by some predetermined

milestone), offer conversion into company equity or other available

assets. If successful, the company could finance their CAPEX needs on

better terms and without diluting shareholders while investors could

gain exposure to high-upside in an otherwise unavailable investment.

Additional benefit could come in broadening company exposure or markets

via this fundraise as well.

For example, imagine an investment into the future revenues of a new

model of SpaceX rocket. The capital intensive requirements for creating

such a technology would typically lead to equity dilution and less

internal control of the business. In an STO raise, SpaceX could engage

the public, find financing on better terms, avoid dilution, and offer

high returns upon the successful commercialization of the product. In

the event of failed commercialization, investors could convert into the

equity of SpaceX at some pre-defined conversion ratio. Compared to the

compromises made via traditional means of financing, this approach could

make sense.

The market will surely mature. A blockchain-based security can

ultimately offer all the features of existing securities with additional

ones - reducing costs and increasing distribution. They are

fundamentally better. However, incremental benefit in an immature

market, like a real estate token, will not catalyze a seismic shift in

capital markets. The potential future benefits for portfolio managers of

real estate is clear, but how to jumpstart this marketplace remains murky. Real estate is just kinda boring.

Regulatory compliance is unavoidable and important, but those in the

industry (myself included) could gain from asking more often, what do

people actually want? The ICO world is imperfect, but the stodgy ethos

of STOs - middle-aged white men in blazers, their lawyers ever by their

side, talking in finance jargon about tranches of multi-asset EB5 blah

blah blah - could benefit from the creativity, boldness, and fun of the

crypto-craze that got us here.

--- The views and opinions expressed are those of the author and do

not necessarily reflect the official policy or position of Atomic

Capital, Inc. This is not intended as investment advice. Any content

provided is not intended to malign any religion, ethic group, club,

organization, company, individual or anyone or anything.

Traditional real-world assets, such as gold, are finding higher liquidity by being tokenized.

Utility tokens have traditionally been the modus operandi for

new blockchain company funding rounds, through the initial coin

offering (ICO). But although utility tokens supposedly have value within

the platform they operate on, they often lack a unique value

proposition and likewise, by definition they do not represent an actual

tangible asset. In fact, utility tokens are so far removed from real

world assets, that the U.S. Securities and Exchange Commission (SEC)

have recently been cracking down on those ICOs which cross the

boundaries into the territory of being a security in their efforts to

provide fundamental value to holders.

This

is one of the main reasons that the value of utility tokens, either

during their token sale or once they are trading on third party

exchanges, is driven predominately pure speculation, rather than the

robustness of their tokenomic model.

However, asset-backed tokens, often offered during a Security Token Offering

(STO) carry an actual value, because they are correlated with an

external, real-world asset’s value. Asset-backed and security tokens

offer secure, rapid and minimal cost trading of traditional assets via

blockchain technology, and increase liquidity for traditional

securities.

Why Make an Asset-Backed Token?

Security

tokens, or asset-backed tokens, increase the potential initial raise

for fund operators and other parties who issue securities. However, the

main reason it’s beneficial for crypto fund managers to create

cryptographic analogues of traditional assets is to increase the

underlying assets liquidity — defined as the ease and speed at which

assets are purchased or sold (liquidated) at market price. Generally,

bonds and stocks are assets with high liquidity, in contrast to assets

such as vehicles, real estate, jewellery, art and collectibles which

lack access to high trading volumes, trading opportunities on exchanges,

and liquidity.

But

why is liquidity so important? Liquidity correlates strongly with an

asset’s trading volume, and subsequently affects that assets price. Good

liquidity can enhance the underlying assets value, as it negates the

risk associated with being unable to exit a position in a given asset

quickly. For example, whilst it’s easy to exit a position in a stock via

a third-party exchange, liquidating your position in a piece of

real-estate is a significantly longer process, as in simplest terms, it

takes longer to find a buyer.

A

tokenized asset trading market which trades 24 hours a day, 7 days a

week and 365 days a year not only provides enhanced price discovery and

reduces price volatility, but it may also reduce the risk of a sudden

price crash in asset value.

An Overview of Asset-backed Tokens Use Cases

Tokens

which are backed by external assets are somewhat comparable to gold

backed paper currencies, like many traditional fiat currencies were

under the ‘gold standard’. But the situation becomes more complex when

we examine tokens associated with assets which are ‘non-fungible’— for

example, real estate.

The

real estate market is fairly illiquid, and heavily afflicted with

multiple inefficiencies; such as middlemen who receive a portion of an

investment for taking on counter-party risk. However, these pain points

could be alleviated and given greater value with asset-backed tokens,

which would tokenize a portion of an individuals position in a

real-estate asset.

The

most novel use cases for asset-backed tokens are therefore emerging

from tokenomic models which are backed by limited liquidity assets —

such as derivatives, private equity, real estate, collectibles, and

other assets which have been traditionally difficult to find immediate

buyers for. Currently, assets which are non-fungible are worth

trillions, but are for the most part they are stored in vaults worldwide

as hedges against inflation rates.

Illiquid

assets aside, the largest use cases for asset-backed tokens, which have

the highest potential to raise funds during an STO, generally manifest

from tokenizing a portion of a large established company’s debt or

equity.

A quick look at some examples of asset-backed token use cases include:

The issuance of corporate debt or equity via a security token.

Real

estate investment trusts (REITs), for investors that wish to diversify

their portfolio to include real estate. Real estate investment trust

tokens would also allow customization, and may be purchased by investors

willing to accept a certain credit risks, for a pre-determined

duration.

Equity

from commercial properties and rental income. Retail investors who have

a relatively modest amount of capital are currently unable to diversify

into the commercial property and rental market. Ownership

fractionalization through security tokens offers the opportunity to

democratize commercial and rental investing.

Intellectual

property asset backed tokens, such as film licenses and royalty

payments, may be distributed to every party who owns a portion of a

patent, film, or book.

Accounts

payable and receivable, represented by security tokens, has the

potential to replace supply chain finance and factoring, with tokens and

data flowing between accounts receivable and accounts payable, in ERP

systems.

Real world assets represented as tokens on the blockchain therefore provides access to potentially large addressable markets.

Smart

contracts associated with tokenized assets may likewise improve access

to trading opportunities. Although professional investors can currently

use the services of lawyers and other service provides to perform due

diligence on new investments, investors with lower capital amounts can

generally not afford to take on such risk. Tokens with built in smart

contracts can automate due diligence to an extent, which in turn has the

potential to open markets to retail investors who lack access to due

diligence providers— creating even greater liquidity.

Likewise,

a private equity backed token can be developed to feature protocols

with inbuilt dividend and profit share functions, transforming an asset

class with traditionally low liquidity into a passive income generating

investment. This offers startups and VC firms a greater opportunity for

funding, cost-savings and profit.

Below, we examine the four main asset-backed token categories in greater detail.

What are the Main Asset-Backed Token Categories?

Fine

art could likewise benefit from asset-backed tokens, allowing

fractionalization of paintings — for example among multiple recipients

of inheritance.

Earlier

we introduced an overview of asset-backed tokens, why you would want to

tokenize an asset, and looked at some of the most obvious use cases for

asset-backed tokens.

Now, we are going to break asset-backed token use cases down further into the following four categories:

Debt and equity tokenization

Asset-Backed Tokens for Commodities

Hard Assets which are Non-Fungible

Soft Assets which are Non-Fungible

Debt and Equity Tokenization

Debt

and equity asset-backed tokens are used predominately for funding

start-up companies, which in turn circumvents intermediaries such as

investment banks and traditional exchanges (for IPOs).

Fractional

ownership for equity isn’t a new concept — stock certificates and

mutual funds have already existed for decades. But what asset-backed

tokens now offer is a percentage digital ownership of an immutable,

liquid and trustless representation of company debt or equity.

Anyone

may access the blockchain protocol on which an asset-backed token

resides, including security token exchanges, and may verify the

ownership of the token and the authority of a specified individual to

trade. Arbitrage opportunities for market makers should maintain an

asset-backed token’s trading closely within its true net value.

Debt

and equity are already assets which can be traded today, but blockchain

makes this process more efficient, which could significantly grow the STO

market. Subsequently, a 50% decrease in price (via destruction of asset

value) could easily be counter-balanced by a thousand percent volume

increase (via creation of new market value). This would assist both

incumbents and entrepreneurs alike, who would need to react quickly

during emerging production and marketing industry shifts, which are

expected to enhance value of company assets and company market share.

Holdings

of private equity funds are most often low liquidity assets which

require investors to hold for over one year. Likewise, hedge funds often

hold assets with relatively low liquidity which often require investors

to hold assets for at least a few months. Therefore, enhanced liquidity

via asset tokenization would increase the value of assets for both

private equity funds and hedge funds, enabling private equity ventures

to adapt easily to market fluctuations.

Tokenization of Commodities

Exchange

traded commodities can likewise be converted into security tokens.

Regardless of whether it’s oil, natural gas, wheat, or sugar,

commodities which are already traded on third party exchanges can be

effectively tokenized.

Trading

of other more fringe commodities, like renewable hydro-electric, wind,

and solar electric energy can also be facilitated through a blockchain

based exchange. As a result, governments, utilities companies, and

individuals could participate and transact together on one platform.

However,

tokens which are backed by physical assets require verification to

establish the tokens validity. A mature market already exists for

auditors who verify the security and trustworthiness of custodial

storage facilities for commodities. Those same auditors could take

advantage of new opportunities using blockchain technology, by utilizing

manual assessment methods in conjunction with blockchain tracking —

relying upon technology to create confidence in the market.

Although

gold commonly trades as paper assets through gold ETFs, gold which has

been tokenized is fundamentally different. Each gold backed token

represents a whole or fraction of a a gold bar which is stored and

audited, through the services of an“oracle” provider, for it’s weight,

purity level, and it’s authenticity — Therefore, those who tokenize gold

or other commodities have to first solve the issues with oracle

providers to realize widespread asset-backed token adoption.

The

leading cryptocurrency, Bitcoin, often referred to as ‘digital gold’,

may potentially be replaced as the primary store of digital value by

using tokenized gold. Current advantages which Bitcoin holds over

physical gold, is it’s relatively easy divisibility and transferability.

For example, it is simple for token exchanges to take 1% of a Bitcoin,

sending the equivalent dollar value of BTC into an individuals

cryptocurrency portfolio.

In

contrast, it is conceivably of far greater difficulty to take a gold

bullion bar, fractionalize it, and send it to an individual. If that

gold bar were to be tokenized, one could easily sell and transfer any

given percentage of gold in a similar way to traditional paper

currencies backed by gold— and the same is true for other real-world

commodities.

Hard Asset Tokenization

Hard assets

are tangible and physical items or objects of worth that are owned by

an individual or company. There are many possibilities for the

tokenization of hard assets on the blockchain.

Tokenization of Real Estate

As

we briefly touched on earlier, when compared to REITs or private

property ownership, real estate token funds could become a borderless,

more profitable, and a more democratic way to invest in things such as a

portfolio of rental properties, senior-care homes, or a hotel chain.

With

the rise of real estate backed tokens and tokenized rental income,

investors of every wealth bracket can build out a diverse and flexible

real estate portfolio with minimal exchange fees.

Collectibles tokenization

Bitcoin’s

are fungible. Every Bitcoin is interchangeable, just as Euros, Dollars,

and Pound Sterling. They are indistinguishable from each other, as they

are all, at their core, units of currency and exchange.

In

contrast, asset-backed tokens have the ability to represent exotic and

non-fungible assets, like collectibles, and therefore they are

distinguishable from one other tokens by design. Each token is unique,

creating digital scarcity, with blockchain network participants knowing

how many are in circulation and their distinguishing features.

The

back-end component of non-fungible asset tokenization for exotic assets

have a sophisticated design. Asset management firms which currently

deal with traditional assets may fill new roles as oracles, ensuring the

back-end of non-fungible tokens are kept in safe storage, undergoing

regular audit certification, asset insurance, and conversion mechanisms

from tokens into a physical asset delivery. Auction houses currently

fill this role with fine jewelry, furniture, art, wine, and other

collectibles.

For

example, as it stands, most retail investors lack the opportunity to

buy an ownership share of a rare piece of artwork. Incumbent auction

houses such as Sotheby’s and Christie’s control a majority of secondary

art markets from the world’s financial centres, far from reach for

retail investors. However, smart contracts are being used to create

joint ownership of artworks or art collections stored in museums. These

artworks can still be displayed publicly, but the asset will be encoded

on a blockchain.

Likewise,

it’s possible for individual objects to be tokenized, acting as

appreciating assets. For example, a rare, valuable painting may be

inherited by several siblings. With asset-backed tokens, the painting

could be tokenized and then distributed to each sibling via the

blockchain, becoming “shares” representing a portion of the original

painting. These shares, represented by asset-backed tokens, could be

sold via a public security token exchange, if a sibling wishes to sell

their holdings. In this simplified example, the token holders have

access to immediate liquidity, while private investors can add a

valuable exotic asset to their portfolio, which they would normally not

have exposure to — therefore, a novel class of exotic assets are given

previously unrealized liquidity.

Non-Fungible Soft Asset Tokenization

Soft assets, in contrast to hard assets, are intangible assets,

which have been traditionally hard to quantify and evaluate.

Asset-backed tokens can likewise bring price discovery and liquidity to

these assets.

Intellectual Property (IP) Tokenization

Somewhat

harder to quantify than other assets we have examined, IP assets, such

as copyright licences, trademarks, patents and royalties from music and

media rights generally have low liquidity and currently lack a secondary

marketplace to trade on. It is not a difficult concept to tokenize the

IP ownership, but the realized benefits could be many — such as enhanced

liquidity and increased value of IP assets, bringing benefits to media

producers and artists.

Digital Asset Collectibles Tokenization

Digital

collectibles, such as CryptoKitties, are examples of asset-backed

tokens which generate value and scarcity. This is in contrast to

ownership of digital collectibles, which is managed via central

databases, such as vanity items earned during whilst playing online

games. These assets have been traditionally difficult to prove ownership

over, as they are often just represented as contracts with the software

provider. However, blockchain could offer digital collectibles

specialized marketplaces, created with asset-backed tokens.

Stable Coins are not Typical Security Tokens

By

certain definitions, stable coins linked to fiat are a form of stable

asset-backed token. Stable coin issuers in this case maintain fiat

reserves, so they retain a stable ratio with their chosen fiat currency,

which is then matched to the circulating supply of the specific stable

coin.

Stable

coins are distinctly different from security tokens as they’re not a

means of investment. Instead, they are created to represent currencies

rather than assets. Stable coins provide an easy exit for investors who

trade cryptographic assets on token exchanges, and remain fundamentally

distinct from security tokens representing assets.

Opportunities and Challenges for Security Tokens

Compared

to traditional currency, Bitcoin has been generally regarded as having

greater fungibility, divisibility, transferability, scarcity, and

durability. Likewise, asset-backed tokens retain most of the same

benefits, applying them to real assets.

Regulators

are eyeing security tokens with caution. There could be high risks for

new user error whilst using exchanges, and investors who are not

cautious may lose their tokens through wallet address mishaps for

example, something protected against when using traditional third-party

exchanges.

As

a result of regulatory uncertainty, some countries, such as China and

Qatar, have completely banned asset-backed tokens being issued. Other

countries, such as Bermuda, Switzerland, Estonia, and Liechtenstein,

allow security token issuance, albeit with certain restrictions and

confusing regulatory oversight.

Malta,

by contrast, places no limitations or restrictions on asset-backed

tokens. Approval, fund certification, and fund license requirements are

legally well-defined, with regulatory stringency. These conditions make

Malta the premier jurisdiction to issue asset-backed or security tokens.

Asset-backed

and security tokens are, by design, prone to lower volatility than

utility tokens and cryptocurrencies. As discussed, tokens listed on

exchanges may trade constantly, offering greatly enhanced price

discovery. Markets which operate irrespective of geographical location

or time zones may provide security token trading opportunities to

investors worldwide. Likewise, established companies may soon begin

issuing security tokens worth billion of dollars into token exchanges —

creating one of the most exciting asset classes seen in decades.

Friday, June 29, 2018

China's penetration of Silicon Valley creates risks for startups

SAN

FRANCISCO (Reuters) - Danhua Capital has invested in some of Silicon

Valley’s most promising startups in areas like drones, artificial

intelligence and cyber security. The venture capital firm is based just

outside Stanford University, the epicenter of U.S. technology

entrepreneurship.

FILE

PHOTO: Stanford University's campus is seen in an aerial photo in

Stanford, California, U.S. on April 6, 2016. REUTERS/Noah

Berger/File Photo

Yet it was also established and funded with help from the Chinese government. And it is not alone.

More

than 20 Silicon Valley venture capital firms have close ties to a

Chinese government fund or state-owned entity, according to interviews

with venture capital sources and publicly available information.

While

the U.S. government is taking an increasingly hard line against Chinese

acquisitions of U.S. public companies, investments in startups, even by

state-backed entities, have been largely untouched.

That may

well be poised to change as the U.S. Congress finalizes legislation that

dramatically expands the government’s power to block foreign investment

in U.S. companies, including venture investments.

The new law

would give the U.S. government’s Committee on Foreign Investment in the

United States (CFIUS) wide latitude to decide what sorts of deals to

examine, eliminating certain ownership thresholds, with a particular

focus on so-called “critical” technologies.

“The perception is

that a lot of the tech transfer of worry to the U.S. security

establishment is happening in the startup world,” said Stephen Heifetz, a

former member of CFIUS and now a lawyer representing companies going

through CFIUS review.

Sponsored

The

latest version of the bill exempts “passive” investors, which would

cover many of the limited partners that back venture firms. But limited

partners that have some control over the business, or firms whose

managing partner is a “foreign person”, could be subject to scrutiny.

The

university endowments and family offices that traditionally provide

most of the money for venture firms are usually one of many limited

partners and have minimal if any involvement in the startups they help

fund.

Chinese entities also sometimes take a passive role in big

venture funds. But venture capital sources say that Chinese government

funds often play a more influential role in the smaller venture firms

they back by providing a greater percentage of their funding. That

empowers them to request information about startups or help them to

open offices in China - potentially opening those startups to CFIUS

review.

The possibility of a regulatory crackdown has caused

unease in the startup world. Venture firm Andreessen Horowitz is

counseling startups that if they raise money from a China-backed

investor, they put themselves at risk of government scrutiny, a person

with knowledge of the matter said.

“The window for some

startups to raise money from China may be closing,” said Chris

Nicholson, co-founder of AI company Skymind, which has raised money from

Chinese Internet group Tencent Holdings Ltd and a Hong Kong family

office.

SENSITIVE AREAS

Until recently, the original

source of funds for venture investments has not been an issue in Silicon

Valley. Venture firms are not obliged to disclose who their investors

are and entrepreneurs rarely ask, leading some dealmakers to question

how CFIUS could keep tabs on startup investing.

Danhua Capital,

which is backed by the Zhongguancun Development Group, a state-owned

enterprise funded by the Beijing municipal government, has holdings in

some of the most sensitive technology sectors.

Its

investments include data management and security company Cohesity,

which counts the U.S. Department of Energy and U.S. Air Force among its

customers. Drone startup Flirtey, which in May was selected by the U.S.

Department of Transportation to participate in projects to help the

agency integrate drones safely into U.S. air space, is also part of the

Danhua portfolio.

Shoucheng Zhang, Danhua’s founder and a

Stanford University physics professor, declined to answer specific

questions from Reuters. In an email, he said: “Most of our (limited

partners) are publicly listed companies in New York or Hong Kong stock

exchanges. We will of course fully comply with any legislations and

regulations.”

Cohesity declined to comment. A spokeswoman for

Flirtey said Danhua’s minority investment did not come with any

information rights or a board seat, and the firm is not involved in

Flirtey’s operations.

“We would not knowingly accept money from

the Chinese government; we take investment from Delaware-registered,

Silicon Valley-based venture capital firms,” the spokeswoman said.

She

added that Flirtey would support any new “mandate that investors must

disclose if they have any form of backing from government entities, to

help ensure there is never a question in the future.”

The

practice of investing through layers of funds, known as funds of funds,

can make it all but impossible to know where money is coming from.

Westlake Ventures, backed by the Hangzhou city government in eastern

China, invests in at least 10 other Silicon Valley venture funds,

including Palo-Alto based Amino Capital.

Larry Li, founder and

managing partner at Amino Capital, said he took the money that was on

offer when he launched his fund in 2012. He said he felt his firm wasn’t

the kind of known quantity that could tap the big pensions and

endowments.

“We weren’t going to the Harvard endowment or Yale

endowment; that’s like mission impossible,” Li said. “You need to have

some special source of funds to get started.”

China-backed

funds include Oriza Ventures, which belongs to the investment arm of

the Suzhou municipal government, and has backed AI and self-driving car

startups. SAIC Capital, the venture arm of state-owned auto company SAIC

Motor, has invested in Silicon Valley autonomous driving, mapping and

artificial intelligence startups.

Even well-known startup accelerator 500 Startups raised part of its main fund from the Hangzhou government.

500 Startups and Oriza declined to comment, while SAIC did not respond to a request for comment.

Capital

controls have slowed the flow of Chinese money into the United States

since 2016, but sources say venture investments have been more resilient

than sectors like real estate, in part due to the Chinese government’s

focus on improving its domestic high-tech industry.

‘CROWN JEWELS’

U.S.

politicians suspicious of China’s intentions were galvanized by a

Department of Defense report released last year that warns that Chinese

venture investors are accessing “the crown jewels of U.S. innovation.”

The

report helped guide Sen. John Cornyn, a Texas Republican who sponsored

the Senate version of the CFIUS reform bill, people with knowledge of

the matter said. A spokeswoman said Cornyn “is especially concerned with

Chinese state-backed venture capital investments.”

But the report was also panned by many private sector experts as overly simplistic and fear-mongering.

For

now, at least, President Donald Trump has backed away from his declared

intention to clamp down on a wide range of Chinese technology

investments through a special emergency order, saying he would leave the

job to CFIUS. But if Congress fails to pass the bill quickly, Trump

said he would use his executive powers.

Reporting

by Heather Somerville in San Francisco. Additional reporting by the

Shanghai newsroom.; Editing by Jonathan Weber and Martin Howell.