Any possibility of a rate hike at the meeting’s conclusion on Wednesday was already crushed under the weight of weak data early in the year. To be sure, the data support the transitory nature of the weakness, justifying Federal Reserve Chair Janet Yellen’s optimism last month, but it remains too little, too late. Instead, turn to September as the next opportunity for the first rate hike of this cycle.

Yellen established her view on the first-quarter data in a May speech:

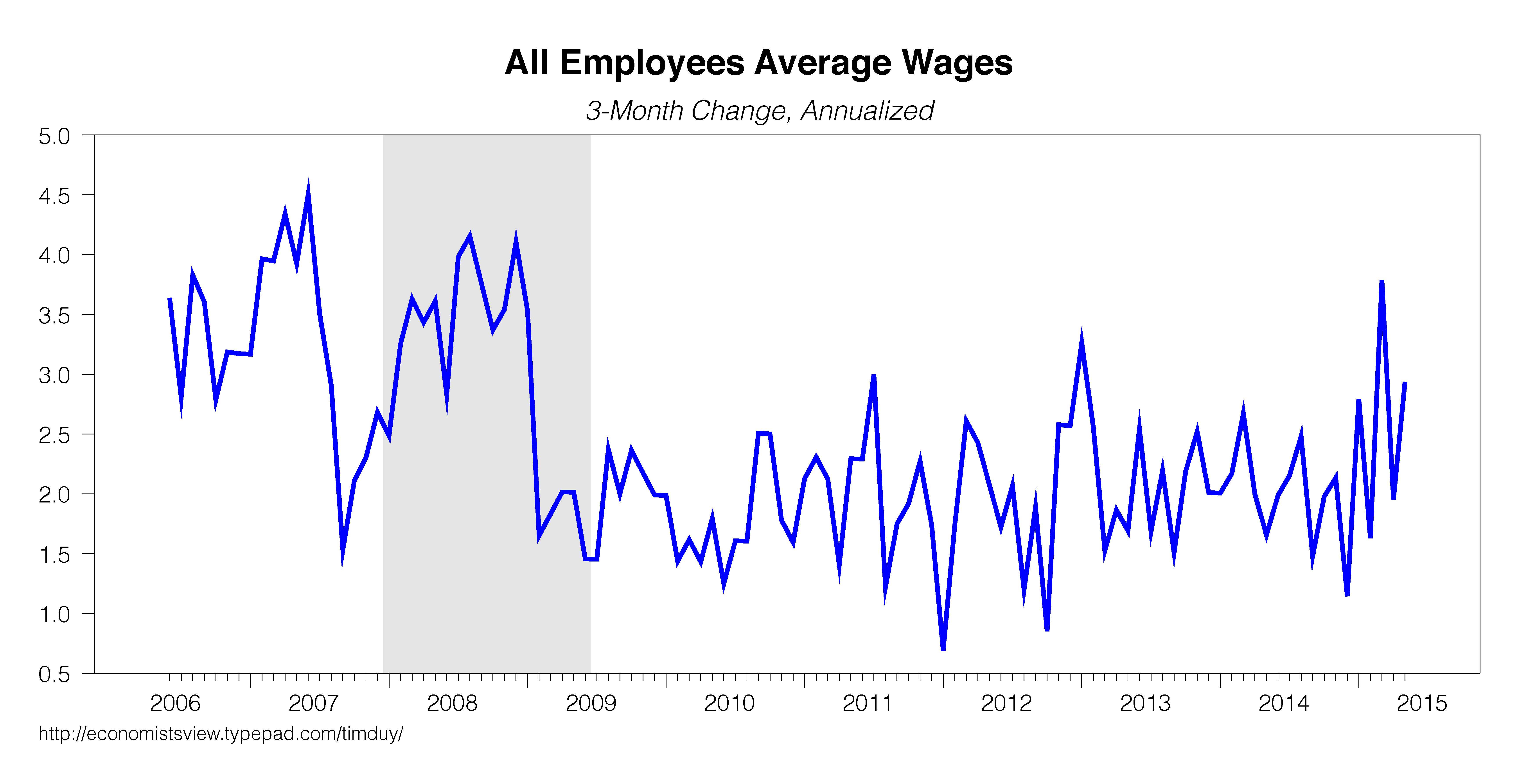

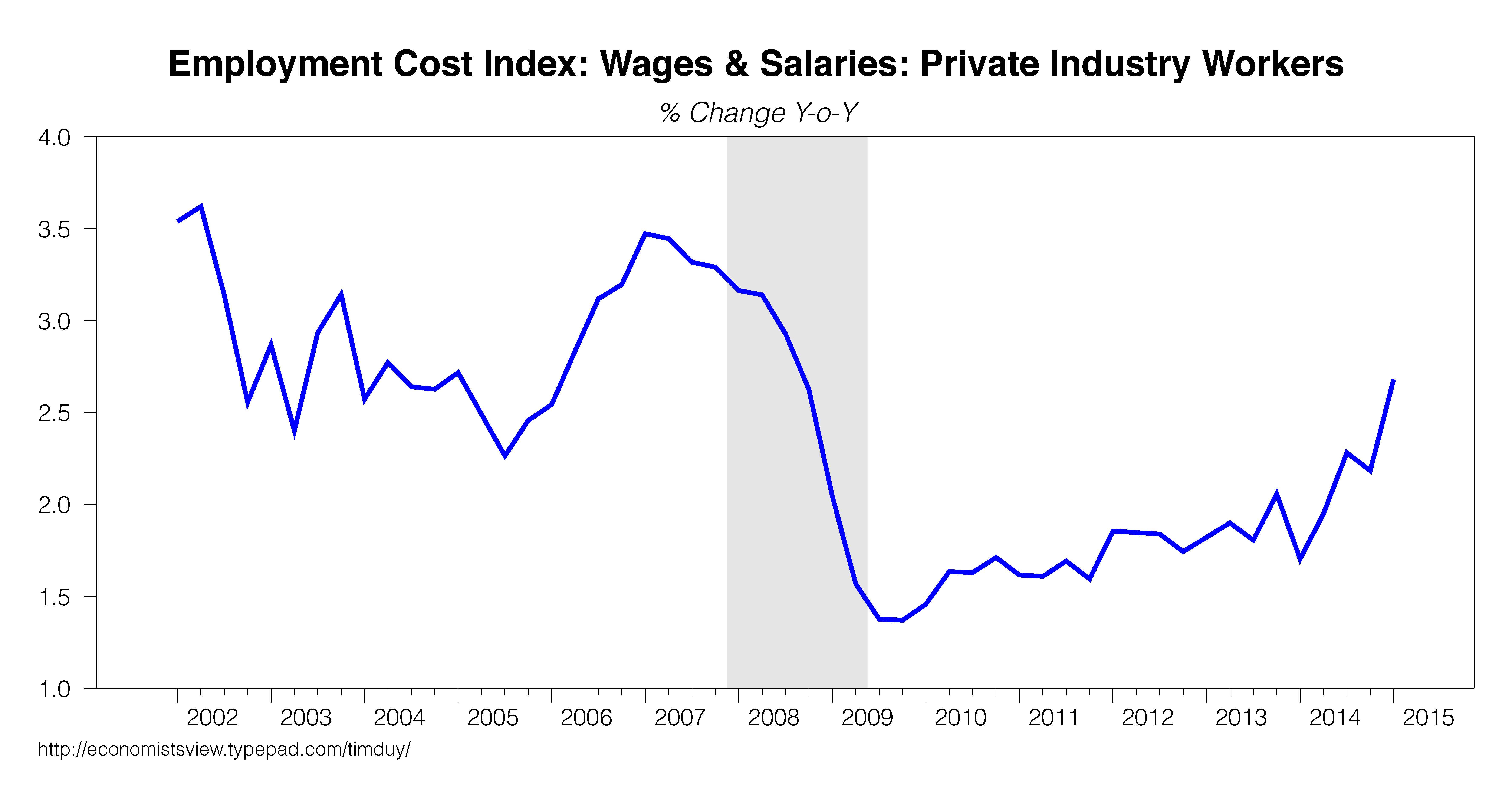

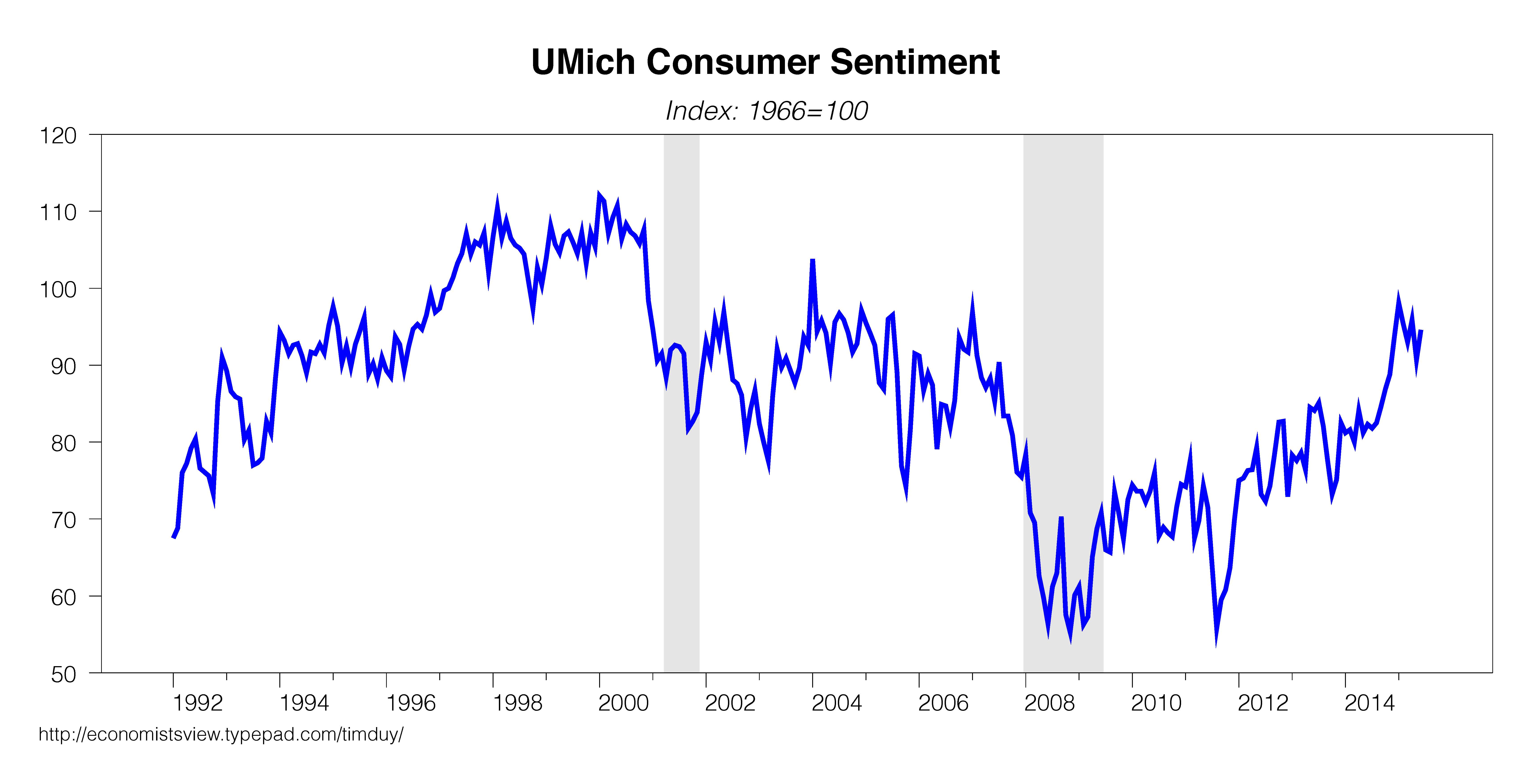

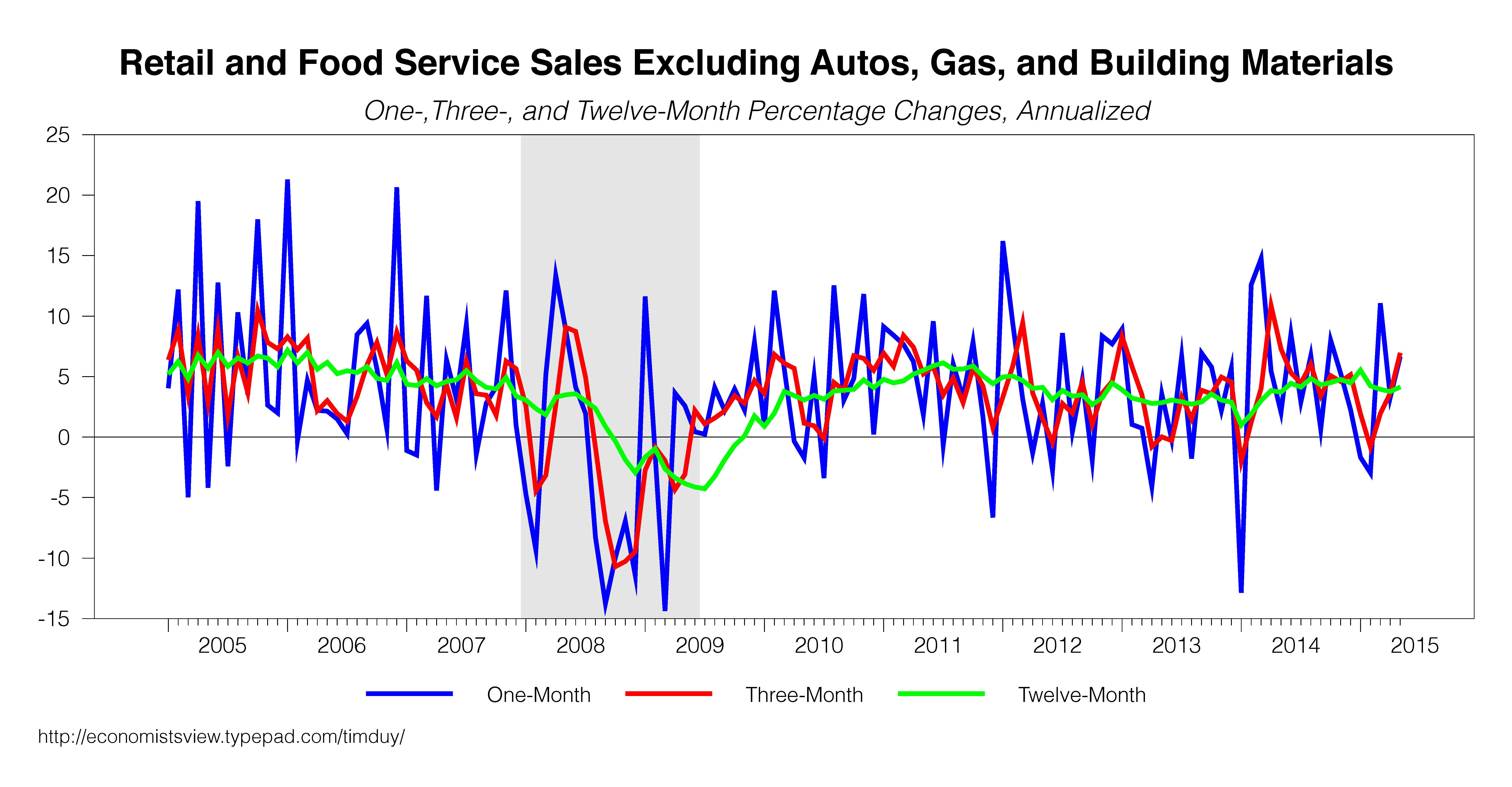

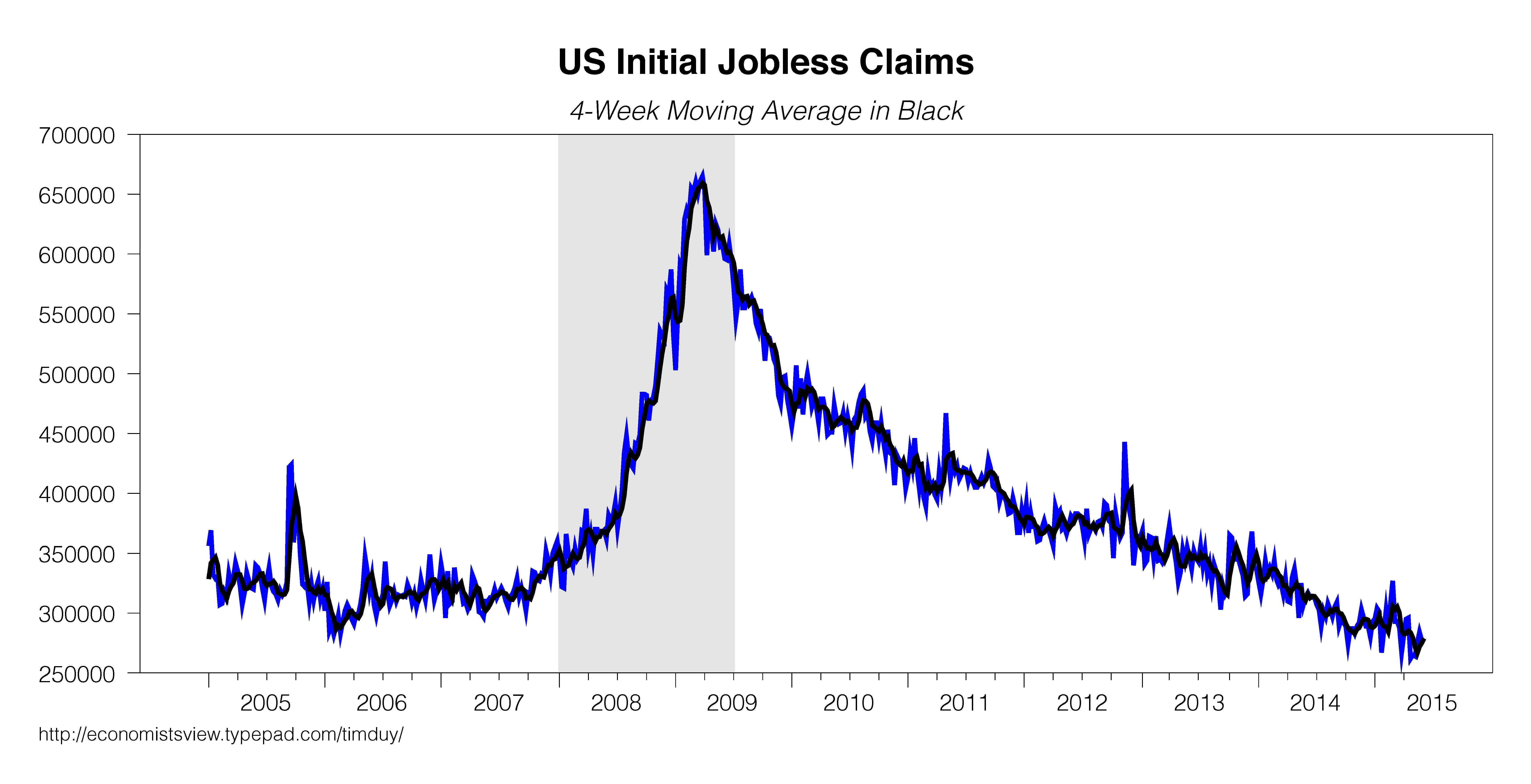

If confirmed by further estimates, my guess is that this apparent slowdown was largely the result of a variety of transitory factors that occurred at the same time, including the unusually cold and snowy winter and the labor disputes at ports on the West Coast, both of which likely disrupted some economic activity. And some of this apparent weakness may just be statistical noise. I therefore expect the economic data to strengthen.Recent data suggest Yellen was correct to trust her instincts. Job growth remains steady, with solid reports for both April and May and even tantalizing hints that wage growth is accelerating:

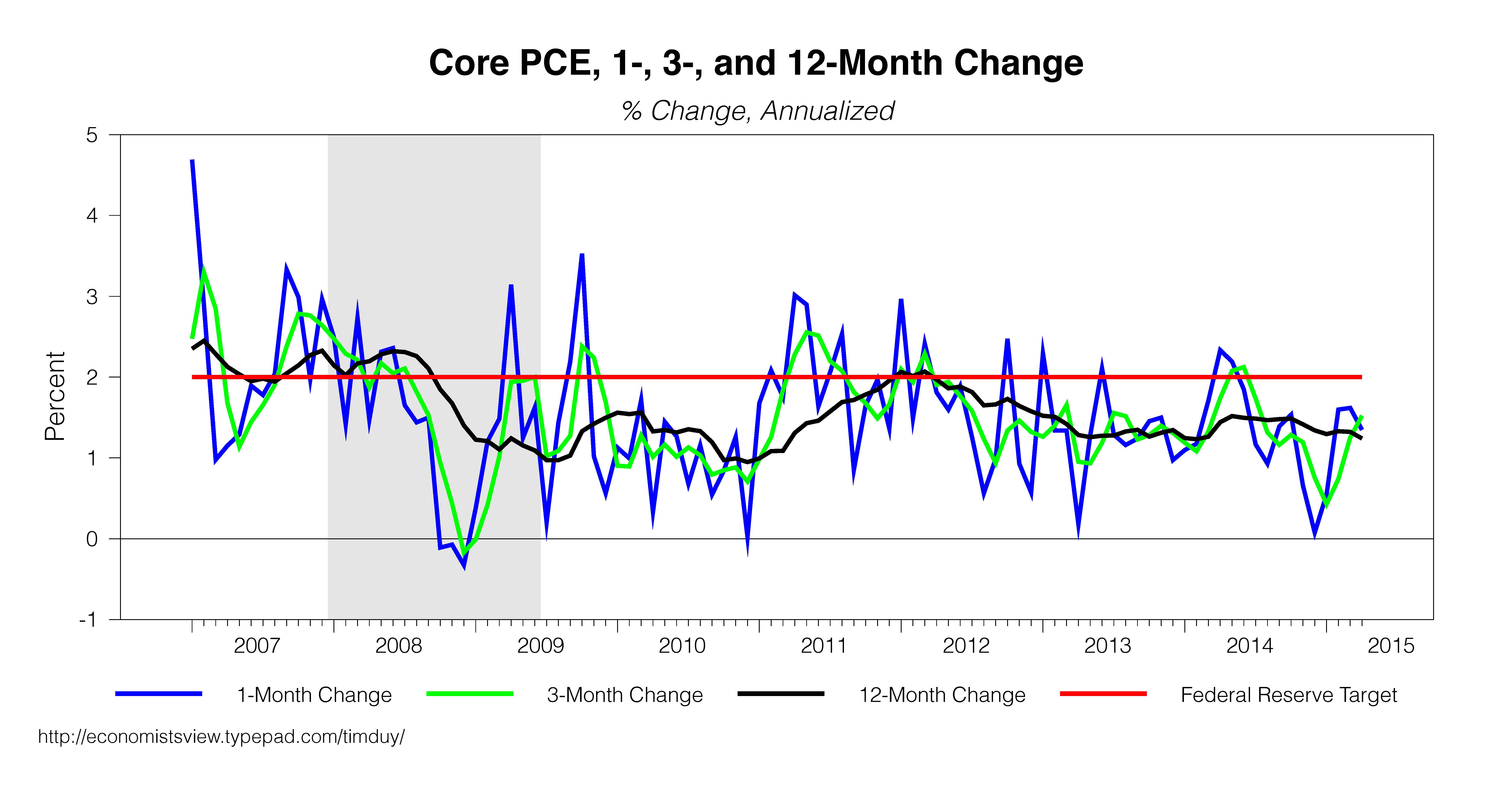

Tim Duy

Tim Duy

Tim Duy

Tim Duy

Tim Duy

Tim Duy

Overall, and not surprisingly, given the spate of better news, the now closely followed Atlanta GDP tracker second-quarter estimates are climbing:

Tim Duy

Tim Duy

The data has been weaker and I think that the markets have appropriately moved back the likely date of policy firming.The ease with which policymakers backed down from a June rate hike speaks to their concerns about the fragility of the economy. They are unwilling to risk undermining the expansion they so carefully helped to nurture, nor do they see pressing reason from inflation data to do so.

Tim Duy

With no change in rate policy, expect changes to the FOMC statement to be limited to the opening description of the economy. There is a possibility of dissent by Richmond Federal Reserve President Jeffrey Lacker, which might create some news, but which I would interpret as mostly noise. More interesting will be the new set of forecasts from meeting participants. Near-term growth forecasts are likely to be reduced in response to the slow start for the year. Modest downward revisions to inflation forecasts could also be expected.

Given the tendency of the Fed to be positively surprised on unemployment, I think they would be wary of downgrading their forecasts of that indicator. What I am watching more closely is any further downward adjustments to long-run inflation forecasts. Considering recent revisions in March, additional revisions would signal that officials are quickly changing their perspective on the natural rate of unemployment—a development with significant implications for the path of interest rates. The rate projections themselves are likely to be revised modestly downward, particularly in the near term. Indeed, the most aggressive rate forecasts for this year seem to have lost nearly all validity, given the lack of any hikes in the first half of the year.

Yellen’s press conference will be the highlight of the day. The Fed’s statement will likely be interpreted as dovish; be wary that Yellen is subsequently interpreted as hawkish as she will reaffirm the case for a rate hike later this year. She will repeat her conviction that policy needs to be forward looking and thus the time to begin normalizing draws near. But she will also reiterate that the path of policy is data dependent, and the current data and forecasts point to a very gradual increase in rates. Policymakers would like this message to shine through the noise; the more-tradable issue of the first rate hike, however, is likely to remain the dominant focus of market participants.

No comments:

Post a Comment